Project Alpha Intelligence Report: May 7, 2026

Project Alpha Intelligence Report: BC Real Estate Development and Macroeconomic Outlook — May 7, 2026

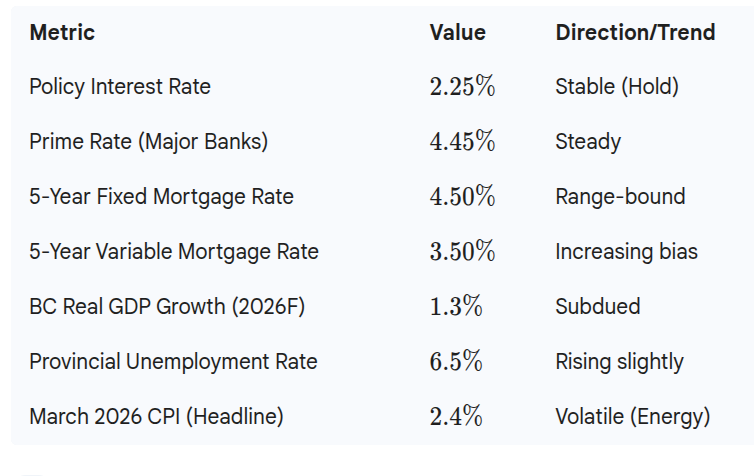

The residential development sector in British Columbia enters the second quarter of 2026 in a state of tentative stabilization, following a multi-year period of significant contraction and structural readjustment. The macroeconomic environment of May 2026 is defined by the Bank of Canada’s continued commitment to a 2.25% policy rate, a stance maintained during the April 29, 2026, announcement amidst persistent geopolitical volatility and trade-related uncertainties. For industry participants, this represents a “higher-for-longer” equilibrium compared to the pre-2022 era, yet a substantial relief from the 5.0% peak observed in 2024. As the provincial economy navigates a sluggish GDP growth forecast of 1.1% to 1.5%, the real estate market is characterized by record-high inventories and a fundamental pivot toward ground-oriented “missing middle” housing and highly amenitized luxury resort products.

The following analysis synthesizes seven critical Real Estate Development Marketing Act (REDMA) filings from May 2026—Main & Park, Silverbrook, Centrale, Cabot 1, Osprey Landing, Eagle Summit Skyline, and the Abbotsford Florence Drive project—within this broader context of shifting demand, evolving regulatory burdens, and stabilizing but elevated construction costs.

Macroeconomic Foundation: The May 2026 Credit and Trade Environment

The primary determinant of project feasibility and buyer engagement in the current cycle is the cost of capital. The Bank of Canada’s April 2026 decision to hold the overnight rate at 2.25% reflects a cautious balance between a cooling domestic economy and external shocks, most notably the conflict in the Middle East and the volatility of U.S. trade policy. While core inflation has receded to approximately 2.3% headline inflation recently spiked to 2.4% driven by a 21% surge in gasoline prices, leading the Governing Council to adopt a “watchful” posture.

Table 1: Key Macroeconomic Indicators — May 2026

For the development industry, this monetary environment has resulted in a “shaky pause” in bond yields, with the 5-year Canadian yield hovering around 3.1%. Developers are increasingly facing a labor market that is “neither hiring nor firing,” with an unemployment rate of 6.7% providing some relief from the labor shortages of previous years, though wage growth remains sticky at 4.7%. The “vibes are bad” sentiment reported by market observers reflects a household sector whose confidence has been eroded by a 30% increase in the cost of essentials since 2021. This has led to a market where end-users are necessity-based buyers, and investor participation remains notably absent, particularly in the concrete condominium segment.

Market Pulse: Shifting Demand and Inventory Glut

As of May 2026, the British Columbia housing market is navigating a “prolonged period of weakness”. Total residential unit sales in March 2026 were down 3.6% year-over-year, while the average provincial price fell 2% to approximately $939,846. The most significant pressure is observed in Metro Vancouver, where sales reached a 25-year low in 2025, and inventory levels have surged to their highest point since 2015.

Table 2: Regional Market Statistics (April 2026)

The Fraser Valley market provides a compelling case study for the “rebalancing” phase. In April 2026, the region recorded 1,118 sales, an 11% month-over-month increase and the first year-over-year gain in over a year. However, with a sales-to-active listings ratio of only 11%, the market remains firmly in buyer’s territory, defined by a 12–20% range for balanced conditions. This buyer advantage is manifesting through aggressive developer incentives, including strata fee subsidies, cash-back credits, and “try before you buy” programs designed to coax hesitant purchasers off the sidelines.

Analysis of Project Alpha REDMA Filings: May 2026

The seven filings analyzed this month represent a diverse array of risk profiles and strategic responses to the current macroeconomic climate. These projects range from 5-unit urban multiplexes to large-scale master-planned townhouse communities and luxury resort residences.

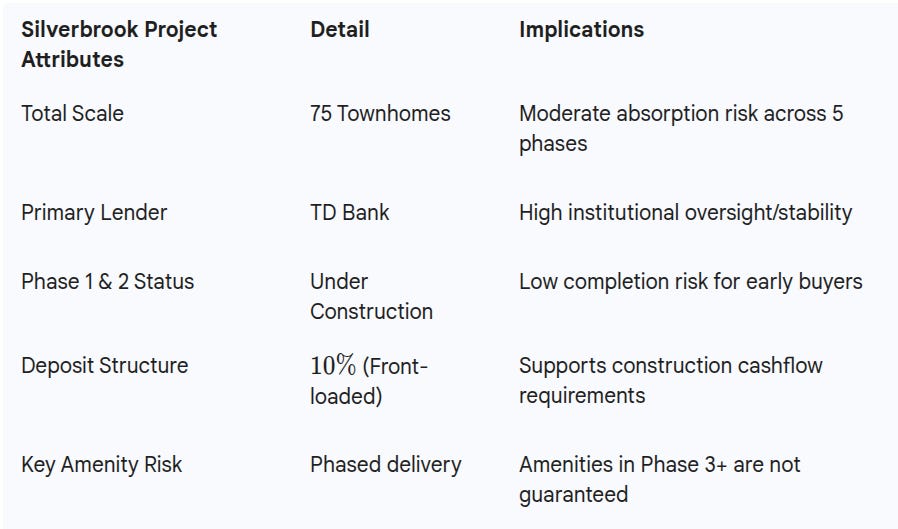

1. Silverbrook (Willoughby, Langley): The Institutional Benchmark

Silverbrook, a 75-unit townhouse development by Royale Properties (208) Ltd., represents the high-water mark for institutional confidence in the May 2026 cohort. Secured by financing from the Toronto-Dominion Bank, the project is structured across five phases to align supply with the currently muted absorption rates in the Fraser Valley.

The project’s financing structure is a notable outlier. Unlike smaller developers reliant on private or related-party debt, Silverbrook’s access to Tier-1 capital indicates a robust pro-forma that has likely already accounted for the 4.5% Average Annual mortgage rate environment. However, the disclosure reveals a highly restrictive assignment policy, requiring the developer’s consent and a fee of either 3% of the purchase price or 50% of the profit “lift”. This mechanism serves to deter speculative flippers and ensure that the project is anchored by end-user equity, a necessity for lenders in a market where “investor participation remained largely absent” in 2025.

The pricing environment for Willoughby townhomes in May 2026 remains competitive. Contemporary listings in the area range from $799,000 for 4-bedroom units to $949,000 for newer completions. Silverbrook must navigate this “inventory glut,” as the Fraser Valley’s total active listings sit 45% above the 10-year seasonal average.

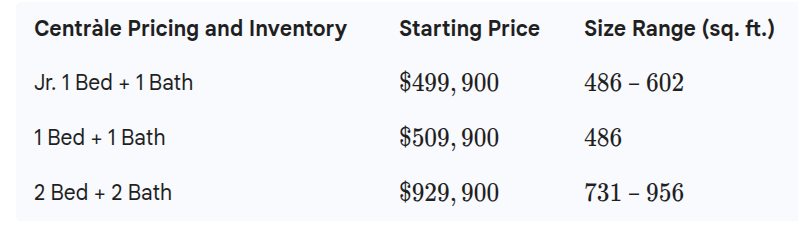

2. Centràle (Burnaby Heights): The Urban Village Feasibility Test

Centràle, located at 4488 Hastings Street, is a 34-unit mixed-use project that serves as a critical indicator of the viability of the “urban village” model in 2026. Developed by a Capitol Hill-specific partnership, the project faces a stringent $50\%$ pre-sale requirement by April 30, 2027, to satisfy its conditional construction financing from Coast Capital Savings.

The developer has introduced aggressive “Grand Opening” incentives to meet this threshold, including $10,000 credits for one-bedroom units and $15,000 for two-bedroom units. This reflects the broader trend where “developers increasingly relied on incentives to support absorption”. With junior one-bedroom units starting at $499,900, Centràle is positioned at a price point designed to capture the “missing middle” demand that has migrated away from high-rise concrete towers.

The project’s risk profile is elevated by the “satisfactory financing commitment” requirement under Policy Statement 6. As of the May filing, the developer had not yet obtained a firm commitment that is unconditional on sales volume. This creates a 12-to-18-month window of exposure for early depositors, whose funds could be tied up in trust while the developer seeks to achieve the 50% sales target in a “soft” market.

3. The Residences at Cabot 1 (Revelstoke): Luxury and the “Rent Charge” Mechanism

The Cabot 1 filing in Revelstoke targets a distinct demographic: the ultra-high-net-worth recreational buyer. Developed by Revelstoke Alpine Village Inc. (affiliated with the Robert Gaglardi family), this 9-unit project is funded entirely from internal developer funds, bypassing the need for third-party pre-sale thresholds.

The project introduces a sophisticated but potentially contentious fiscal mechanism: a “Rent Charge” of up to 0.3% of the fair market value annually, enforceable via power of sale. When combined with a mandatory rental management structure, the project functions more like a hospitality asset than traditional residential strata. This aligns with the “Mountain Road Estates” strategy in Revelstoke, where luxury duplex villas start at $4 million and attract global buyers looking for “lifestyle residences” that can support rental use.

Revelstoke’s recreational market remains “strong” in May 2026, with single-family property values forecasted to increase 5% this year despite a 6.5% drop in the condominium median price to $750,000. The Cabot 1 project capitalizes on the “limited supply” of slope-side inventory, where house prices often start at $4 million.

4. Osprey Landing (Wardner): The Receivership Signal

The Osprey Landing disclosure represents a critical market signal: the “monetization of distressed assets.” Deloitte Restructuring Inc., acting as the court-appointed receiver for KS Property Management Inc., is marketing the final 13 lots of an 80-lot bare land strata subdivision. The receivership was triggered by a default on $15.3 million in debt to Kootenay Savings Credit Union following a failed divestment of shares mandated by the BCFSA.

This filing provides a sobering look at the “tail-end risk” of recreational developments. The infrastructure was completed in 2012, yet the project has been “listed for sale over several years with two different realtors” without achieving total sell-out. The “as-is, where-is” purchase conditions and the receiver’s right to 100% of the profit on any assignment highlight the limited leverage available to buyers in distressed environments.

The presence of builders’ lien claims totaling over $2.5 million on related lands (Twin River) further underscores the “execution decay” that can occur when developer liquidity vanishes. For industry analysts, Osprey Landing is a reminder that even “completed” projects carry significant legal and operational risks during a credit contraction.

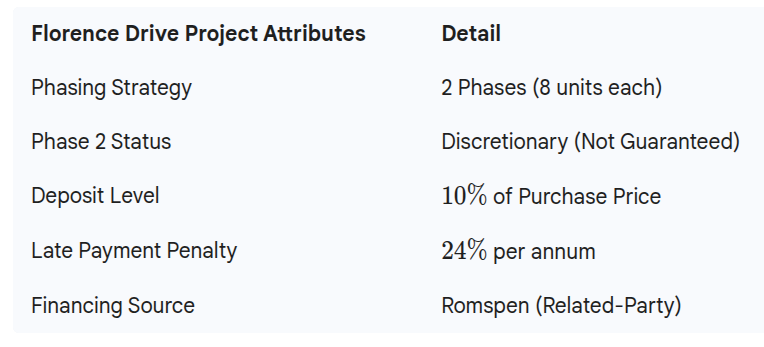

5. Abbotsford Phased Townhouse Project (Florence Drive): Phasing and Risk Mitigation

Liberty Ridge Homes Inc.’s 16-unit townhouse project at 36545 Florence Drive illustrates the “cautious recovery” model. By phasing the project into two 8-unit buildings, the developer reduces its immediate capital requirements while using a related-party lender (Romspen Investment Corporation) to bypass institutional rigidities.

A high-signal item in this filing is the 24% per annum interest rate on late payments, which is substantially higher than the standard 10%–15% seen in more balanced cycles. This “penalty-driven” structure reflects a developer’s need for absolute certainty in closing dates to service high-interest construction debt. Additionally, the 50% strata fee subsidy for Phase 1 indicates that “absorption support” is necessary even in established suburban submarkets.

The BCREA’s April 2026 forecast expects Fraser Valley home sales to drop by 4.5% this year before a projected 9.1% rebound in 2027. Liberty Ridge’s decision to make Phase 2 “future and discretionary” is a direct response to this “stagnant economy” and the uncertainty of when “pent-up demand” will actually re-materialize.

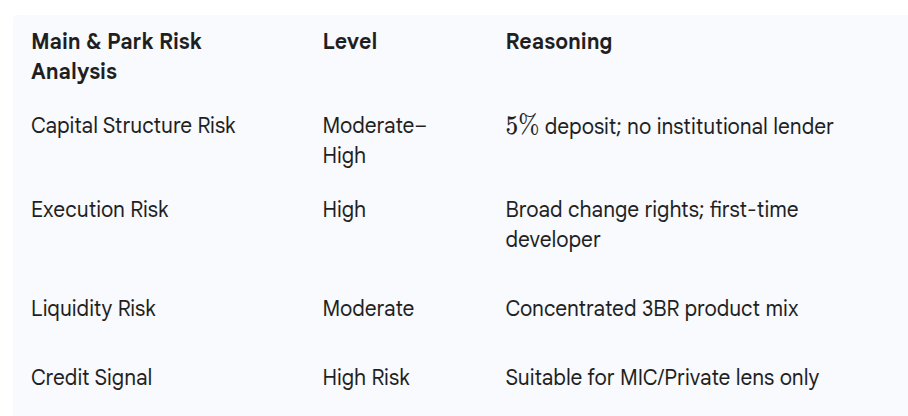

6. Main & Park (Vancouver): The Small-Scale Multiplex Risk

Main & Park, a 5-unit strata development at 164 & 166 East 38th Avenue, represents the “micro-development” trend fueled by Vancouver’s recent zoning changes. However, the May 1, 2026, filing reveals a high-risk profile for a first-time developer entity (Deso Properties).

The disclosure grants the developer “extremely broad” unilateral rights to change unit sizes, count, layout, and materials without triggering rescission rights, provided the changes are not deemed “material”. Furthermore, the 5% deposit structure is significantly lower than the 15% to 20% typically required for urban projects, which may attract buyers but provides a thin cushion for the developer against defaults.

With 3-bedroom units in East Vancouver starting at $1.38 million (based on comparable 2-bedroom prices of $1.03 million), the Main & Park project must compete with “standing inventory” that offers immediate occupancy and less execution uncertainty.

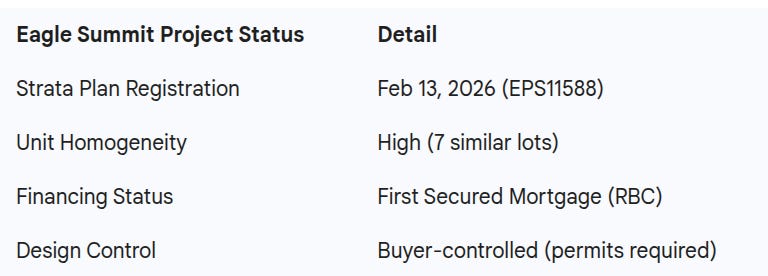

7. Eagle Summit Skyline (Abbotsford): The Bare Land Strata Pivot

Eagle Summit Skyline (35276 Eagle Summit Drive) presents 7 bare land strata lots, a product type that has gained popularity as developers seek to offload vertical construction risk to the end-user. Backed by the Royal Bank of Canada, the project is “fully approved” and the strata plan was registered in February 2026, meaning the development risk is largely behind the sponsor.

The primary insight here is the “shift of inflationary pressure.” By selling lots rather than finished homes, Eagle Mountain Properties is insulated from the 2.8% annual increase in residential construction costs. The buyer, however, must navigate a market where “skilled labor shortages” remain the primary challenge and “retaliatory tariffs on steel” continue to drive up material costs.

Regulatory and Fiscal Headwinds: SVT and BCFSA Policy Shifts

The May 2026 filings are the first to operate under the “higher-for-longer” regulatory regime of the BC government. Two primary policy shifts are currently reshaping developer pro-formas and buyer behavior.

The 2026 Speculation and Vacancy Tax (SVT) Increase

Effective January 1, 2026, the SVT rates have doubled for Canadian residents and increased by 50% for foreign owners. This has significant implications for pre-sale absorption and “holding” strategies.

The provincial government has attempted to offset the impact for residents by increasing the homeowner tax credit from $2,000 to $4,000, but for the “investor class” that previously drove the pre-sale market, the cost of an “empty” unit has become a prohibitive carrying expense. This has contributed to the “soft condo resale market” and the shift of newly completed units into the rental pool, which nearly doubled the 10-year average in 2025.

BCFSA REDMA Policy Statements 5 and 6

The British Columbia Financial Services Authority (BCFSA) has refined the “Early Marketing Period” requirements to better reflect the difficulty of obtaining municipal approvals in 2026. Under the new Policy Statement 5, developers can commence marketing once a rezoning bylaw passes third reading, rather than requiring a full development permit.

Furthermore, the BCFSA launched a pilot program on February 25, 2025, allowing projects with 100 or more units to extend their early marketing period from 12 to 18 months. While none of the May analyzed projects currently meet this unit threshold, the policy indicates a system-wide recognition that the “lifecycle of a development” has been extended by high construction costs and municipal “red tape”.

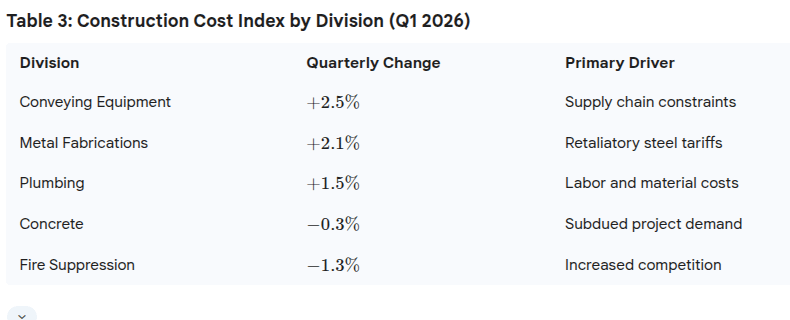

Construction Cost Trends and the Supply-Chain Frontier

Developers in May 2026 are operating in an environment of “stabilized inflation,” yet costs remain at a historically high baseline. The first quarter of 2026 saw a 0.6% increase in residential building costs, following a 0.5% rise in Q4 2025.

Table 3: Construction Cost Index by Division (Q1 2026)

The “metal fabrications” spike is a direct result of the U.S.-Canada trade friction, where tariffs on steel have been expanded to avoid “circumvention”. For wood-frame projects like Main & Park or Silverbrook, these costs are more manageable than for concrete high-rises, which are facing cost ranges of $500 to $750 per square foot in Vancouver. This cost disparity is the primary driver of the “condo correction” and the pivot toward townhomes, where costs in Surrey range from $320 to $420 per square foot.

Synthesis: The “Alpha” Signals for May 2026

The convergence of the macroeconomic data and the specific REDMA filings reveals several “High-Signal” trends for the remainder of the 2026 calendar year.

The Financing Barbell: There is a growing divide between institutional-grade developments (Silverbrook, Centrale) and those reliant on related-party “bridge” debt (Main & Park, Florence Drive). Projects with non-bank financing often carry higher interest penalties for buyers and broader “change rights” for developers, signaling a need for enhanced due diligence.

Inventory as a Strategy: The “Osprey Landing” receivership and the “Eagle Summit” bare-land model suggest that the most successful “plays” in 2026 are those that either monetize existing inventory or offload the vertical construction risk to the buyer.

The “Rent Charge” Precedent: The Cabot 1 filing introduces the “Rent Charge” as a tool for long-term resort viability. If successful, this model may proliferate in other BC resort communities (Sun Peaks, Big White) as a way to circumvent the volatility of traditional strata-fee-only funding.

The Absorption Ceiling: With the Bank of Canada holding at 2.25% and mortgage rates range-bound at 4.5%, there is a clear “absorption ceiling” for luxury and investor-grade products. This is being bridged by “Marketing Crutches” like strata fee subsidies and price credits, which protect the “headline price” while providing “carrying-cost relief” to stretched buyers.

Conclusions and Future Outlook

The BC real estate landscape in May 2026 is one of “measured recovery” and “fundamental rebalancing”. The transition away from high-rise speculative development toward ground-oriented “missing middle” housing is well-supported by the cost structures of the BTY Group and the demand profiles seen in the Silverbrook and Centrale filings.

However, the “shadow risk” of current inventory levels cannot be ignored. With 9,816 active listings in the Fraser Valley alone and a “condo glut” weighing on Metro Vancouver growth, the market remains firmly in favor of buyers who possess the liquidity to navigate current borrowing costs. The 2026 SVT increases and the “vibes are bad” economic sentiment will likely keep prices flat to modestly declining through the summer, before “pent-up demand” and a stabilizing trade environment potentially trigger a rebound in 2027. For developers, the mantra of May 2026 is realism over optimism, as evidenced by the high pre-sale thresholds and phased delivery strategies analyzed in this report.